European Endoscopy Devices Market Research Report

- Report Code: EN 1002

- Publish Date: Upcoming

The European endoscopy devices market is mainly driven by favorable reimbursements in selected regions in terms of geography, growing aging population, and increasing prevalence/incidence of diseases. The market value of endoscopy procedures was $7.7 billion in 2013 and is expected to be $9.9 billion by 2018, at a CAGR of 5.20%.

The report “Endoscopy Devices Market Forecast, 2008-2018”, analyzes the market of devices into four segments such as endoscopes, endoscopic visualization system, endoscopic accessories, electronic and mechanical instruments. With a market value of $3.2 billion and $2.9 billion, endoscopes and visualization system have been contributing 41.2% and 38.2% share in terms of total European endoscopy devices market.

The demand for endoscopy has increased because of patients’ preference for minimally invasive surgeries. Endoscopic procedures are low-risk procedures and are easily covered by health insurance. A pivotal factor that propels the growth of the endoscopy market is the rapid rise in the number of elderly people who are prone to orthopedic, gastrointestinal, and ophthalmic, diseases as well as cancer. As per the World Health Organization (WHO), between 2000 and 2050, the proportion of the world's population that is aged 60 years will double from about 11% to 22%. This aging population is the main end-user of knee-hip implants, bariatric surgeries, gastrointestinal endoscopy, and colonoscopy procedures. With the growing number of elderly people, age-related ailments are also expected to rise sharply, thus propelling the demand and consumption of endoscopy devices concomitantly.

The number of people in the world who are obese or overweight has risen to 2.1 billion from 875 million in 1980. Further, approximately 7 million people in the United States have some symptoms of gastro esophageal reflux disorder (GERD). Primary or secondary GERD diagnosis increased by an unprecedented 216 percent or from a total of 995,402 individuals diagnosed in 1998 to 3,141,965 in 2005. 4.2 percent of all people hospitalized with GERD in 2005 also had an esophageal disorder. In the United States, 1,150 deaths in 2004 were directly related to a primary diagnosis of GERD.

North America and Europe both are likely to witness a demand for endoscopes as a result of technological advancements as well as improved reimbursement status in both the regions. Aging population, increased obesity rates, and growing incidence of associated disease are some of the major factors driving the European endoscopy market. Many European countries like England, Germany, and France are witnessing a rise in the number of endoscopic surgeries performed. From 2011 to 2012, more than 360,000 colonoscopies and over 217000 sigmoidoscopic processes were performed in England alone. Further, the department of health in England has predicted a 10% to 20% year-on-year increase in the demand for endoscopies. Bowel scope screening is expected to have a positive impact on the endoscopy market in U.K.

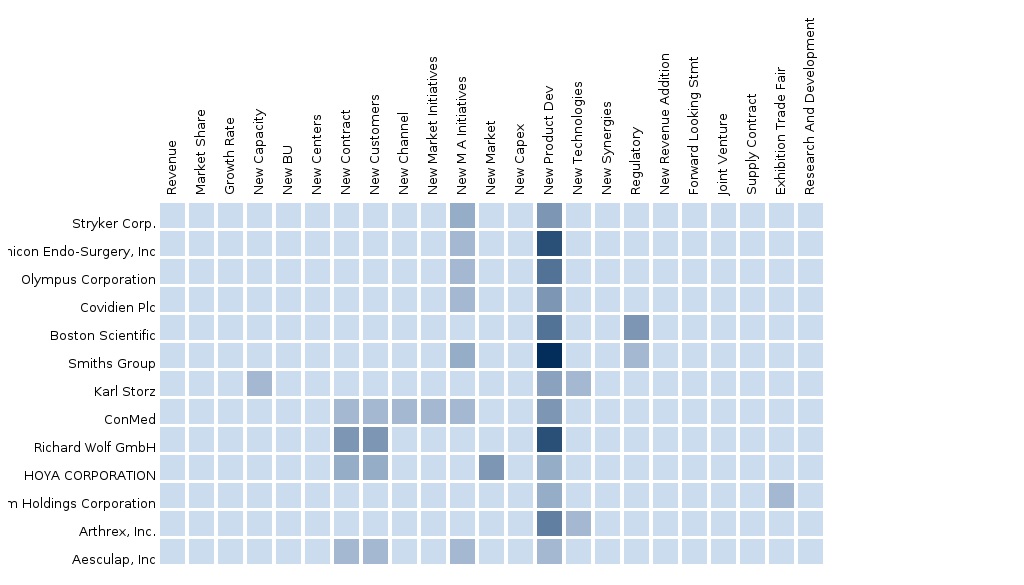

The report provides an extensive competitive landscaping of companies operating in this market. The key players of the market covered in the report are Stryker Corporation, Ethicon Endo-Surgery, Inc., Olympus Corporation, Covidien Plc, Boston Scientific, Arthrex, Inc., Smiths Group, Aesculap, Inc., Karl Storz, ConMed, Richard Wolf GmbH, HOYA CORPORATION, and Fujifilm Holdings Corporation. The details of the segment and country-specific company shares, news and deals, M&A, segment-specific pipeline products, product approvals, and product recalls of the major companies is also covered in the report

Customization Options

Along with the market data, you can also customize MMM assessments that meet your company’s specific needs. Customize to get comprehensive industry standard and deep-dive analysis of the following parameters:

Product Analysis

- Usage pattern (in-depth trend analysis) of products (segment-wise)

- Product matrix which gives a detailed comparison of product portfolio of each company mapped at country and sub-segment level

- End-user adoption rate analysis of the products (segment and country wise)

- Comprehensive coverage of product approvals, pipeline products, and product recalls

Epidemiology Data

- Country-specific prevalence and patient pool of cancer, gastrointestinal tract disorders, gastro esophageal reflux disorder (GERD), gynecological disorders.

- Disease progression (pattern analysis)

Procedure Volume Data

- Different types of endoscopy procedures performed annually in Europe tracked till sub- segment level.

- Number of abdominal, gastro intestinal, interior of joints, gynecology, bronchology, large and small intestinal procedures performed by endoscopy in Europe.

Surgeon's/Physician's Perception Analysis

- Fast turn-around analysis of surgeons response to market events and trends

- Surgeon's opinion about products from different companies

- Surgeon's qualitative inputs on epidemiology date

Brand/Product Perception Matrix

- Comprehensive study of customers perception and behavior through our inbuilt social connect tool checking the virality and tonality of blogs

- Analysis of overall brand usage and familiarity and brand advocacy distribution (detractor/neutral/familiar)

Pricing Trends

- Cost Analysis of endoscopy devices in Europe.

- Procedural investments in Europe for abdominal, gastro intestinal, interior of joints, gynecological, bronchological, large and small intestinal endoscopy.

Competitive Intelligence

- The company share analysis of the top players of the market in the region.

- The crucial developments and strategies of companies inculcating in their portfolio.

1 Introduction

1.1 Objective of the study

1.2 Market Definitions

1.3 Market Segmentation & Aspects Covered

1.4 Research Methodology

1.4.1 Assumptions (Market Size, Forecast, etc)

2 Executive Summary

3 Market Overview

4 Endoscopy-Europe, By Applications

4.1 Laparoscopy-Europe

4.2 GI Endoscopy-Europe

4.2.1 GI Endoscopy-Europe, By Technologies

4.2.1.1 Smart Pill Technology (SPT)-Europe

4.3 Arthroscopy-Europe

4.4 Gynecological Endoscopy-Europe

4.5 Urology Endoscopy-Europe

4.6 Bronchoscopy-Europe

4.7 Mediastinoscopy-Europe

4.8 Otoscopy-Europe

4.9 Laryngoscope-Europe

5 Endoscopy-Europe, By Products

5.1 Endoscopes-Europe

5.1.1 Endoscopes-Europe, By Types

5.1.1.1 Rigid Endoscopes-Europe

5.1.1.2 Flexible Endoscopes-Europe

5.1.1.3 Surgical Endoscopes-Europe

5.1.1.4 Capsule Endoscopes-Europe

5.2 Electronic Endoscopic Instruments-Europe

5.2.1 Electronic Endoscopic Instruments-Europe, By Products

5.2.1.1 Insufflators-Europe

5.2.1.2 Endoscopy Fluid Management Systems-Europe

5.2.1.3 Endoscopic Ultrasounds (EUS)-Europe

5.3 Mechanical Endoscopic Instruments-Europe

5.3.1 Mechanical Endoscopic Instruments-Europe, By Segments

5.3.1.1 Biopsy Forceps-Europe

5.3.1.2 Graspers-Europe

5.3.1.3 Snares-Europe

5.3.1.4 Trocars and Cannulae-Europe

5.3.1.5 Endoscopic Implants-Europe

5.4 Endoscopic Accessories-Europe

5.4.1 Endoscopic Accessories-Europe, By Products

5.4.1.1 Cleaning brushes-Europe

5.4.1.2 Overtubes-Europe

5.4.1.3 Biopsy valves-Europe

5.4.1.4 Endoscopy Carts/Trolleys-Europe

5.4.1.5 Surgical dissectors-Europe

5.4.1.6 Needle holders/forceps-Europe

5.4.1.7 Light cables-Europe

5.4.1.8 Mouth pieces-Europe

5.4.1.9 Fluid flushing device-Europe

Please fill in the form below to receive a free copy of the Summary of this Report

Please visit http://www.micromarketmonitor.com/custom-research-services.html to specify your custom Research Requirement

| PRODUCT TITLE | PUBLISHED | |

|---|---|---|

|

|

Brazil Medical Devices Peers of Brazil medical devices are Orthopedic Devices, Ophthalmology devices, Endoscopy and Neurology Devices comprising 12.8%, 9.2%, 7.2% and 1.9% respectively of the Global Medical Devices market. It is segmented on basis of endusers and... |

Nov 2015 |